Introduction

For the last several decades, the notion that the U.S. payment system’s interchange structure is broken has drawn passionate arguments from many in the payments world. The recent U.S. Senate hearing on the Credit Card Competition Act (CCCA) has stoked this fire with heated arguments both in favor and in opposition.

We argue the system is indeed broken and offer a solution to fix it. We start with a short (and simplified) overview of payment transaction flow and participants to help readers understand the basics. We then determine if the existing U.S. payments framework is “broken” and, if so, articulate what aspects are broken and why. Finally, we suggest a solution to resolve the major issues driving the heated discussions while maintaining the existing economics for participants.

Background

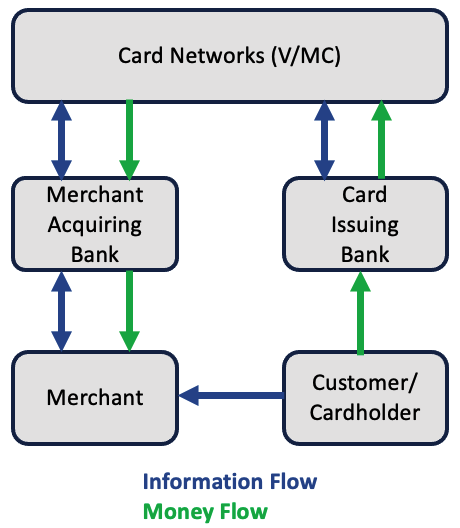

To make payments happen, money and information flow between the parties. The following is a highly simplified representation of the parties and flows.

Competition

Consumers have a choice when it comes to card payments. They can choose from credit cards issued by more than 80 banks and debit cards from almost any bank or credit union.

What’s missing? Competition between card networks to attract merchants. There is none – merchants have little choice but to accept V/MC.

Card Acceptance Costs

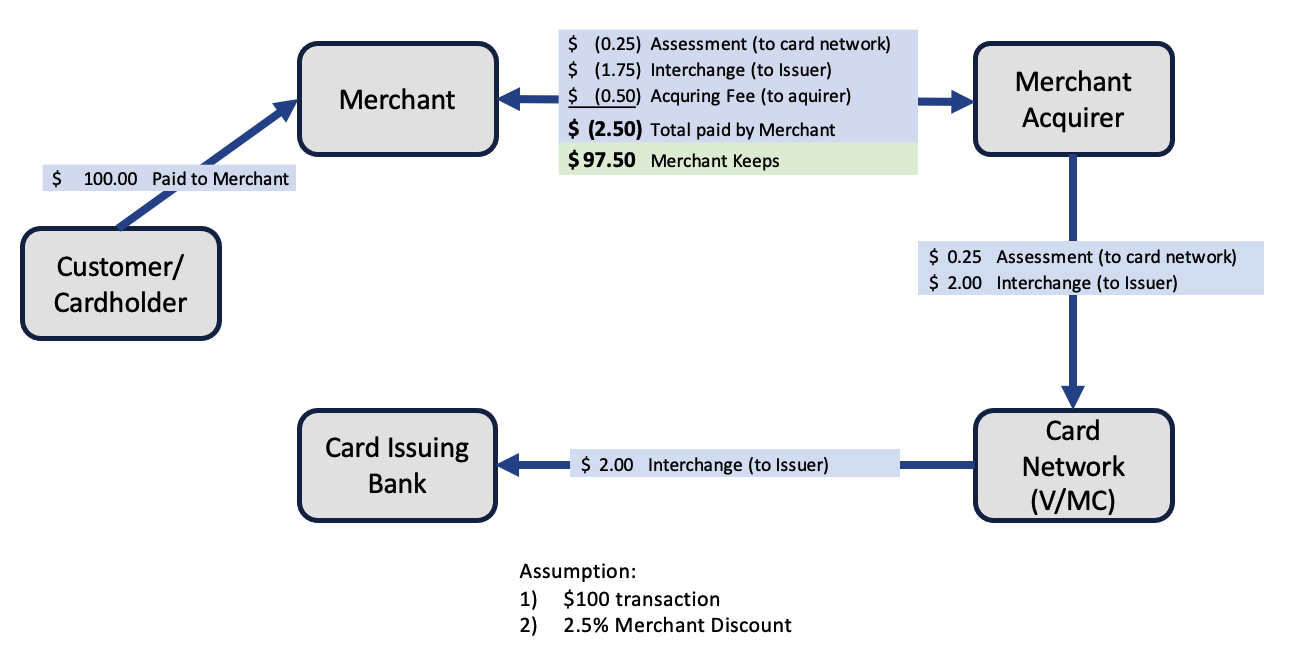

Every business has costs, and someone must pay. In the payment card world, the costs are known as the “merchant discount” or “swipe fees”, and it is the merchant that pays them. The visual below provides a high-level breakdown.

Source: David True

In short, about 80% of the total amount paid by the merchant is set by Visa and Mastercard, with most of that being interchange. One point that is clear from this arrangement: rewards cards cost the merchants more.

For example, a customer purchasing the same goods and services from the same merchant may unknowingly add costs of $0.26 or $2.50 into the system through the choice of payment (regulated debit card or rewards credit card).

If this doesn’t seem fair, you’re right. If it doesn’t seem like a competitive market, you’d be right again.

This is a broken system.

Efforts to Reduce Card Acceptance Cost

Merchants don’t like this broken system, and over the years have tried in different ways to reduce their card acceptance costs:

- Litigation – there have been (and are) several antitrust lawsuits in the U.S. accusing V/MC and Issuers of anti-competitive behavior, such as illegal price setting, including the suit over interchange filed in 2005 and a lawsuit brought by Block in July of 2023.

- Legislation – the Durbin Amendment to the Dodd-Frank bill regulates the cost of debit card acceptance and became law in 2010; the Credit Card Competition Act, meant to extend some features of the Durbin Amendment to credit cards, has been introduced twice in the US Senate.

- New products– MCX, founded in 2012, was a failed attempt to create a merchant-owned and operated payment network.

At best, these attempts have been marginally successful.

Recap and Recommendation

So, how to reduce the merchant cost burden and insert competitiveness into the system? We argue the best way would be to formalize a system that allows merchants – at their option – to pass the transaction-specific cost of cardholder rewards to customers.

How would this work?

1 – Federal law would be enacted that allows all merchants to surcharge for payment card transactions. The surcharge would be limited to the actual interchange that the merchant would pay for the specific transaction, less the regulated debit interchange cost for the same transaction. The law would preempt all state and local laws, card operating regulations, and provisions in merchant agreements that would prohibit or limit surcharging.

2 – When first tendering any payment card, the acquirer/processor would return the actual amount of interchange in excess of the regulated debit cost for that transaction. If merchants wish to increase the amount of the sale by this incremental interchange cost (i.e., surcharge), the merchant would be required to inform the customer of the surcharge amount and allow the customer to affirmatively accept the surcharge or cancel the transaction and provide an alternate payment method for the transaction.

3 – If the customer cancels the transaction, the merchant would send a reverse authorization request for the authorized amount, and the issuer would reverse any authorization hold on the consumer’s account.

By David True and Dean Sheaffer

Author’s Note: This article is excerpted from the following, which dives more deeply into the topics presented: https://www.broadlycurious.com/the-interchange-conundrum-a-novel-solution/